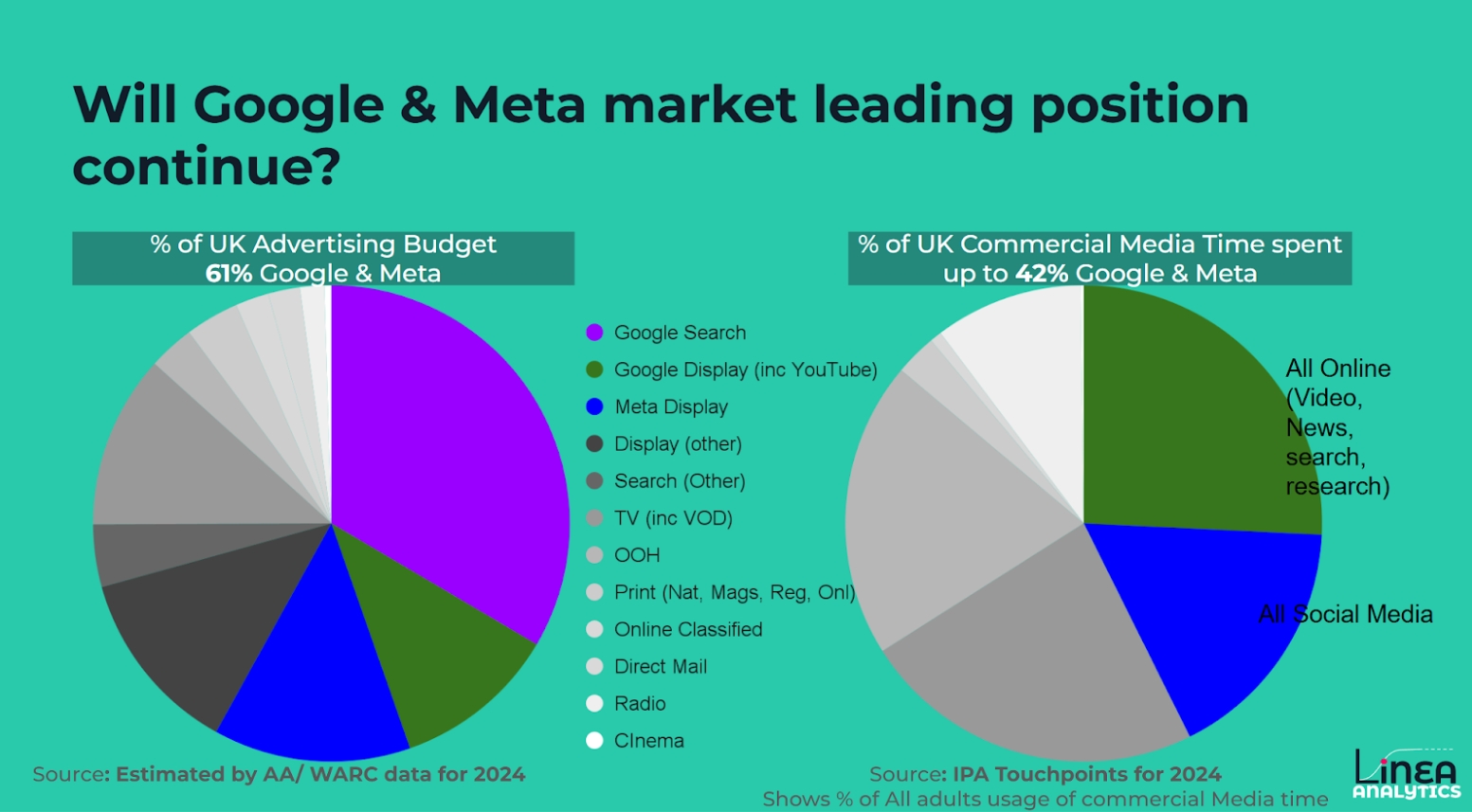

Should UK brands be allocating 61% of their media budget to Google and Meta?

As of 2024, Google and Meta receive 61% of UK media spend. The latest IPA TouchPoints survey shows they account for just 42% of our media time.

How did they come to dominate the UK advertising market?

They grew the market.

In 2007, UK marketing spend was £17bn. Today, it’s £42bn. Had it

simply tracked inflation, we’d be closer to £30bn. So yes, they’ve taken share from traditional channels

(sorry, newsbrands), but they’ve also expanded the pie.

They built better products.

Historically, ad spend followed attention. Google and Meta

earned it. With products that were innovative, engaging, and often habit-forming. Search, in particular, was a

game-changer. Like a modern Yellow Pages, it matched advertising to expressed interest, not just passive time

spent.

A data-driven position

Why target broad demographics on TV when you can reach specific

audiences with precision? We handed over our data and they built targeting engines that delivered measurable,

efficient reach. Marketers could now report on exact customer segments and how many new customers they were

driving. Even when taking into account incrementality, at Linea, we see Meta & Google products are some of

the most efficient channels.

They broadened the market.

Google and Meta made advertising more accessible. Meta alone

has over 10 million active advertisers, many of them small businesses. They didn’t just dominate big brands;

they gave smaller players a seat at the table.

All this highlights how Google & Meta dominated the market.

So, will their dominance continue into the future?

Let's look at three areas that could impact the ongoing dominance of the US tech giants.

1. Moving beyond last-touch measurement

The 2010s were driven by the belief that

marketers could track everything directly. In hindsight, that promise was overstated. Today, brands are

rightly asking two key questions:

- How do we measure incremental impact? MMM & experiments have been the go-to.

- Should platforms be measuring the effectiveness of their own ad spend?

As the shift towards incremental measurement has accelerated, so too has investment in Google and Meta. Suggesting that even under greater scrutiny, these platforms still perform.

2. Have you heard of AI?

There’s been plenty of speculation about how AI could disrupt

search behaviour. But Google Search still posted 12% revenue growth in Q2. Any change will be gradual. Google

still owns the brand, the default position in consumers’ minds, and the integration into our daily

tools.

For challengers (like ChatGPT) to gain ground, they’ll need to outperform, rebrand the

category, and be seamlessly accessible.

3. The rise of new attention formats

Influencers, podcasts, TikTok, and ad-funded models

on platforms like Spotify and Netflix all present credible threats in the battle for attention and, therefore,

ad spend.

Even in an AI-powered world, some things won’t change: people will still watch, listen, and read. And advertising will follow those behaviours. The real question is: who will capture that attention best?

What does the future look like?

Whether Google and Meta continue to outperform will be central to the measurement work we do at Linea Analytics. What matters most is ensuring that ad spend follows the effectiveness of marketing channels, whether that leads to Google, Meta, or emerging platforms.